Note: If you would prefer the audio version of Investing Insights click here to listen to our podcast Episode 4: Are Mutual Funds A Good Investment?

In this quarter’s Investing Insight, I am going to answer the important question, are mutual funds a good investment? Let me cut to the chase…no they are not. Mutual funds are the sacred cow of the largest investment firms, believe me, I do not make any friends among investing peers when talking about this topic. However, I have always believed that investment decisions should not be driven by the status quo within the industry, but that any investment approach should be able to stand up to the rigors of evidence-based analysis.

It is no secret that I am not a fan of mutual funds. I do not like their tax inefficiency, their commonly excessive fees, the lack of intraday liquidity, but most importantly, I do not like the investment strategy of mutual funds. Most mutual funds pursue the investment strategy of stock picking, often referred to as “active management”, which involves a portfolio manager using their “proprietary investment process” to pick the best stocks that they believe will outperform their chosen benchmark index. For example, a mutual fund that buys large cap U.S. stocks will try and outperform a large cap U.S. stock index like the S&P 500 by picking large cap U.S. stocks that the portfolio manager believes will increase in price more than the index average. The goal of course, is to generate additional or excess return above simply investing in the benchmark index fund, which buys all the stocks in the benchmark index. It is important to note that this discussion focuses exclusively on mutual funds that pursue an active management or stock picking approach. Many mutual funds are index funds or have other special investment purposes and I am excluding those funds from this discussion and analysis. Also, stock picking is a strategy that is often performed outside of mutual funds, where investors pick stocks directly in a brokerage account with similar goals as an actively managed mutual fund. Regardless of the investment vehicle used or the approach taken I look at all manners of stock picking with skepticism and you will soon see why.

Active management is the most popular investment strategy deployed in the investment management industry, so why do I dislike it so much? My answer is straightforward, I do not believe there is any evidence that portfolio managers can consistently outperform by picking stocks, and when they do have periods of outperformance, statistics demonstrate that the outperformance is better explained by luck than skill of the portfolio manager. Believing that a portfolio manager has a unique system or process that successfully predicts which stocks will generate the highest returns is the same as believing in market gurus. Plain and simple, I do not believe anyone can predict the price movement of a stock. Having spent years working in investment management firms that manage active stock picking mutual funds, I will tell you a dirty industry secret, most mutual fund portfolio managers also do not believe it is possible to predict the price movement of a stock. Here is a great quote on this topic by Ralph Wagner, a well-known mutual fund portfolio manager.

For professional investors like myself, a sense of humor is essential. We are very aware that we are competing not only against the market averages but also against one another. It’s an intense rivalry. We are each claiming that, ‘The stocks in my fund today will perform better than what you own in your fund.’ That implies we think we can predict the future, which is the occupation of charlatans. If you believe you or anyone else has a system that can predict the future of the stock market, the joke is on you.

Wanger, Ralph. “A Zebra in Lion Country: the ‘Dean’ of Small-Cap Stocks Explains How to Invest in Small, Rapidly Growing Companies Whose Stocks Represent Good Values.” A Zebra in Lion Country: the “Dean” of Small-Cap Stocks Explains How to Invest in Small, Rapidly Growing Companies Whose Stocks Represent Good Values, Touchstone, 1999, pg. 14.

I do not inform the investment decisions I make on behalf of our clients based solely on my lack of faith in investment gurus or stock picking models, and I am not asking you to either. My distaste for active management, like all the investment decisions I make, is built on a foundation of statistical evidence. It is my strongly held belief that investors need to change how they evaluate investment decisions entirely. Active management tries to meet investment objectives by managing future returns. Investors go in search of mutual funds that have had the highest recent returns and then projecting those returns forward they make assumptions about their likely future portfolio returns. This is a strategy doomed for failure. Investors should instead make investment decisions by actively managing the risk of making poor decisions that could result in lower long-term returns. Simply put, because the future is unknowable, investors should focus on making investments that have the highest probability of superior long-term performance, not on making investments that have recently performed the best.

In deciding whether investing in mutual funds and an active management approach is a good investment decision, we need to look at the probability of picking a mutual fund that will outperform and then evaluate the chances that the outperformance will persist over the long-term.

The odds of picking a winning mutual fund

Morningstar puts out a semi-annual analysis called the Active/Passive Barometer which measures the success that active mutual funds have had in beating an appropriate benchmark index. For example, the performance of all active mutual funds that invest in large cap U.S. stocks are compared to the composite performance of many U.S. large cap index funds. The percentage of actively managed mutual funds that beat the benchmark of index funds over different time periods can then be evaluated. This comprehensive analysis shows us the odds of producing better performance by investing in actively managed mutual funds versus simply investing in one or more of the appropriate benchmark indexes.

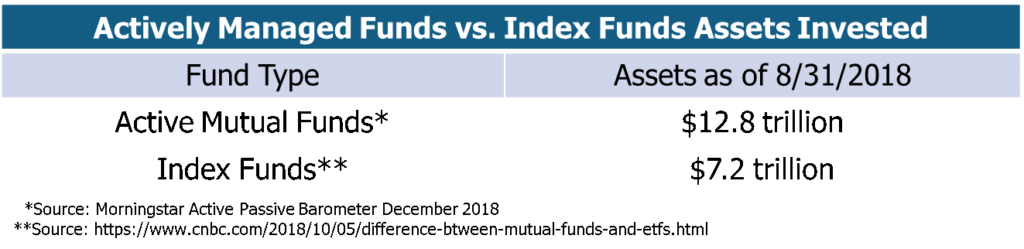

I hate to jump the gun here, but you should know that the results of this analysis have been consistently bad for actively managed mutual funds and that trend continued in latest analysis as of the end of 2018. The analysis covered 4,600 unique actively managed mutual funds that account for $12.8 trillion in assets. Only 38% of the mutual funds survived and outperformed their appropriate benchmark index in 2018! The news for actively mutual funds gets worse, the longer the time period measured, the worse the results. Over the past 10 years ending December 2018, only 24% of active mutual funds beat their appropriate benchmark index over the time period. These results demonstrate that you would have had a 38% chance of picking a winning fund at the beginning of 2018 and only a 24% chance of picking a winning fund 10 years ago. These look more like Las Vegas odds than odds with which investors should make consequential long-term financial decisions.

Investors had a 68% chance of earning higher returns by investing in an index fund in 2018 rather than an active mutual fund, and a 76% chance of earning higher returns from investing in an index fund instead of an active mutual fund over the last 10 years. When you cannot predict the future, it helps to evaluate probabilities of making different decisions, especially when the results year after year remain consistent, which the Active/Passive Barometer analysis has.

The odds that outperformance will persist

Most investors are long-term investors, even if they are in retirement,

they plan to hold securities in their portfolios for ten years or more. It is

not enough to be invested in an active mutual fund that outperforms a few

years, to be better off investing in an active mutual fund instead of an index

fund, outperformance must be consistent over multiple time periods. When I

evaluate securities to include in 3Summit investment strategies, one of the

most important characteristics I look for is persistence of performance. Persistent

outperformance for active mutual funds is really a measure of luck versus

skill. If a portfolio manager can consistently outperform you might be able to

attribute their success to skill versus simply luck as indicated by

inconsistent outperformance.

The S&P Dow Jones Indices compiles a

bi-annual analysis called the SPIVA Persistence Scorecard[1],

which measures how persistent or consistent the performance of the top active

mutual funds ranked by performance have been.

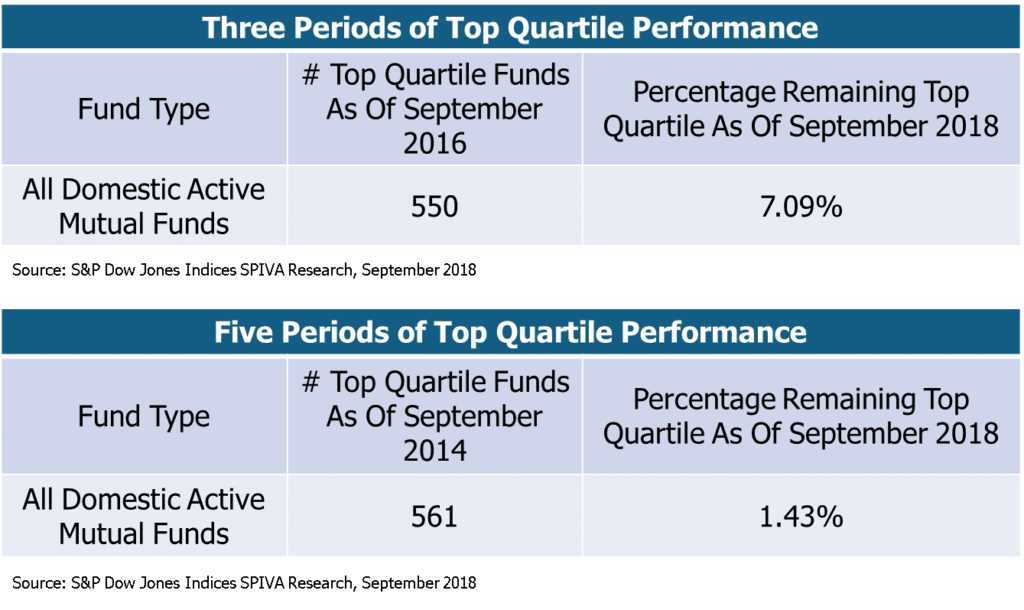

The analysis takes the top quartile (top 25%) of actively managed mutual

funds ranked by performance in September of 2014 and September of 2016 and

calculates the percentage of these top performing mutual funds that are still

in the top quartile performance ranking in September of 2018. Below are the results.

The results of the Persistence Scorecard analysis are striking because they demonstrate no evidence that top ranking actively managed mutual funds can persistently generate top quartile ranking performance. Of the top 25% of actively managed mutual funds in terms of performance, only 7% of the funds remained in the top quartile performance ranking after three consecutive years and only 1.4% remained in the top quartile performance ranking after five consecutive years.

When we began this discussion, I made the statement that I do not believe there is any evidence that actively managed mutual funds can generate persistent outperformance, and when they do, it cannot be explained by skill. Looking at the Persistence Scorecard results, you may think I have overstated my position given that 7% of top quartile funds were still ranked in the top quartile after three consecutive years. However, when you consider the fact that the outperformance could just be random, it appears there is no such thing as portfolio manager skill in the mutual fund universe. If each of the 550 top performing fund portfolio managers as of September 2016 flipped a coin twice in a row representing the next two consecutive years with one side of the coin saying “outperform” and the reverse side saying “underperform”, you would expect given the probabilities of random coin flips that 25% of the portfolio managers would flip outperform twice in a row. These are the odds of being lucky and remaining in the top quartile over three consecutive years. However, only 7% of the managers that where in the top quartile in September of 2016 remained in the top quartile in September of 2018, showing lower odds than even a random outcome.

The bottom line on active mutual fund investing

We have seen that investors would have had a 38% chance of randomly selecting an active mutual fund in January of 2018 that would have outperformed an appropriate benchmark index at the end of 2018. We have also seen that if you bought and held an active mutual fund ten years ago, the odds of that fund beating its appropriate benchmark index is just 24%! Many investors argue these odds can be overcome by analyzing active mutual funds past performance to identify the managers with the greatest skill and investing in that manager’s fund. However, what the Persistence Scorecard analysis shows us is that picking active mutual funds with the best recent performance is an even worse strategy than just randomly selecting an active mutual fund and hoping to outperform. Had you picked a top quartile mutual fund in September of 2016, there is only a 7% chance that fund will still be a top performing fund in September of 2018. As the holding period gets longer the odds get worse, had you selected a top quartile mutual fund in September of 2014, there was a 1.4% chance the fund you selected would still be a top quartile performing fund in September of 2018.

Most investors, even sophisticated investors, pick active mutual funds exclusively based on recent past performance (usually the trailing 3 and 5 year peer performance ranking), believing performance is the best indicator of portfolio manager skill. The Persistence Scorecard analysis demonstrates just how ineffective this strategy is for investors. Out of the active funds in the top quartile performance ranking in September of 2016, almost 20% of those funds where in the bottom quartile of performance rankings by September of 2018. Of the funds in the bottom quartile of performance ranking in September of 2016, more than 12% were in the top quartile of performance ranking in September of 2018. Similar results for each bi-annual Persistence Scorecard analysis indicates these outcomes are most likely not a fluke, but persistent over time. In fact, active mutual fund performance looks like a random walk over time and picking top performing managers has yielded lower odds of success than simply flipping a coin. Given these odds it is hard to make an argument for stock picking and active mutual funds as a prudent investment strategy if your objective is to invest with the highest probability of generating the best returns possible.

Why are active mutual funds so popular?

Actively managed mutual funds continue to manage far more assets than passive index funds.

Why do so many investors try to beat the perilous odds of investing in active mutual funds when all evidence points to the fact that their investment decisions are most likely going to result in inferior short-term and long-term returns? Sadly, I believe the primary reason is that conflicts of interest are rampant in the investment management industry.

A large percentage of investment advisors are not fiduciaries. Non-fiduciary advisors are not required to act solely in their clients’ best interests or clearly disclose their conflicts of interest. Advisors who are not bound by the fiduciary standard, frequently enter into what are called fee-sharing agreements with mutual fund providers. Fee-sharing agreements provide advisors additional fees that are usually minimally disclosed and are paid to them by the mutual fund companies in return for investing their clients’ assets in the mutual fund company’s funds. This type of arrangement can be very lucrative for advisors and for that reason may cause advisors to ignore all the analysis we have reviewed.

Fee-sharing agreements are a serious conflict of interest because they incentivize advisors to make investment decisions on behalf of their clients based not on the quality or merits of an investment, but instead on the total amount of fees they will earn from their clients’ investment accounts. The fact that a large percentage of advisors are not fiduciaries may help understand why active mutual funds remain so popular, and it is not because they are good investments.

[1] Liu, Berlinda, and Aye Soe. “SPIVA Persistence Scorecard.” S&P Dow Jones Indices SPIVA Research, Sept. 2018, https://us.spindices.com/documents/spiva/persistence-scorecard-march-2018.pdf